Investing in Small and Medium-sized Enterprises (SMEs) can be an attractive option for Limited Partners looking for investment opportunities. SMEs can offer the potential for high returns and a chance to support emerging businesses and the broader economy. However, potential downsides also need to be considered before making any investment decisions. We at Winterberg Group know a lot about investing in small and medium-sized companies (SMEs). We can also help Limited Partners understand the good and bad things about this type of investment. The Winterberg Group, led by Co-Founder and Executive Director Fabian Kroeher, has been a critical player in SME investing, providing essential support and guidance to Limited Partners (LPs) looking to capitalise on this growing market. However, investing in SMEs has unique challenges and rewards like any investment strategy. This article will explore the pros and cons of investing in SMEs for Limited Partners focusing on the Winterberg Group approach to SME investment.

The Pros of Investing in SMEs for Limited Partners

High Growth Potential

SMEs often exhibit more significant growth potential compared to larger, more established companies. Smaller businesses can scale rapidly as they are more agile and better equipped to adapt to changing market conditions. For Limited Partners seeking high returns on investment, SMEs can offer a lucrative opportunity.

Portfolio Diversification

Investing in SMEs allows Limited Partners to diversify their investment portfolios, reducing the risk associated with concentrating investments in a single industry or asset class. By allocating capital across multiple small businesses operating in different sectors, LPs can mitigate the impact of market volatility and enhance their portfolio’s overall stability.

Access to Innovative Business Models

Private equity investors have a unique opportunity to tap into the innovative potential of SMEs. These dynamic companies are often at the forefront of developing cutting-edge products and services that can disrupt established industries. Limited Partners can gain access to new markets and technologies by investing in SMEs, positioning themselves for long-term growth.

Economic and Social Impact

Investing in SMEs benefits the individual investor and contributes to economic growth and job creation. SMEs are the backbone of many economies, accounting for a significant share of employment and GDP. By supporting the development of these businesses, Limited Partners can positively impact the broader economy.

Expert Guidance from Winterberg Group

With the support of experienced firms like Winterberg Group, Limited Partners can navigate the complexities of SME investing with greater confidence. Fabian Kroeher and his team offer a wealth of knowledge and expertise helping LPs identify promising investment opportunities and manage their portfolios effectively.

The Cons of Investing in SMEs for Limited Partners

Higher Risk

SME investments can carry a higher risk level than investments in larger, more established companies. Small businesses often face unique challenges, such as limited access to capital, making them more vulnerable to economic downturns and financial stress. As a result, Limited Partners should be prepared to accept a higher degree of risk when pursuing SME investments.

Illiquidity

SME investments are generally less liquid than investments in publicly traded companies. This is because shares in small businesses are not typically traded on a public exchange, making it more difficult for investors to sell their holdings quickly and easily. Limited Partners should be prepared to hold onto their SME investments for an extended period, as they may need more liquid assets to exit the investment.

Limited Information and Transparency

SMEs are often held companies, so they are not subject to the exact disclosure requirements of publicly traded corporations. This can make it challenging for Limited Partners to access accurate and timely information about their investments’ financial health and performance. To mitigate this risk, LPs should work closely with experienced firms like Winterberg Group, which can provide valuable insights and due diligence support.

Management Risk

The success of an SME investment is heavily influenced by the quality of the company’s management team. In some cases, small businesses may need more experienced leadership or have limited resources to attract top talent. Limited Partners should carefully assess the management capabilities of any SME they are considering investing in, as this can significantly impact the potential return on investment.

Regulatory and Compliance Challenges

SMEs may face unique regulatory and compliance challenges, particularly as they navigate the complexities of cross-border operations and international expansion. Limited Partners should know these risks and work closely with firms like Winterberg Group, which can provide expert guidance on navigating the evolving regulatory landscape.

Winterberg Group and Investing in SMEs

Winterberg Group is an investment firm that specialises in supporting SMEs. Founded by Fabian Kroeher – Co-Founder and Executive Director of Winterberg Group – the firm provides funding and support to SMEs in their early development stages. Winterberg Group works closely with SMEs to offer guidance and expertise to help them succeed. Investing in SMEs through the Winterberg Group can allow limited partners to benefit from the potential high returns of SMEs while minimizing the risk. Winterberg Group conducts extensive due diligence on each SME before investing, ensuring that the company has the potential to succeed. Winterberg Group also provides ongoing support to the SME, helping to ensure that the investment is successful. Winterberg Group’s investment strategy is centered around long-term value creation. The firm actively manages the businesses they invest in, working closely with the management team to help drive growth and create value. Winterberg Group’s expertise in the SME sector allows them to identify investment opportunities that have the potential to yield high returns.

Conclusion

Investing in SMEs offers Limited Partners a unique set of rewards and challenges. While the potential for high growth and diversification is appealing, investors need to know the risks associated with this asset class. By partnering with experienced firms like Winterberg Group, led by Fabian Kroeher, Limited Partners can make informed decisions and capitalise on the exciting opportunities presented by the world of SME investing.

“At Winterberg Group, we take a strategic approach to investing in SMEs, focusing on businesses with strong growth potential and a clear path to profitability”, says Fabian Kröher, Executive Director at Winterberg Group.

A record $12.8 trillion assets under management (AUM) in private equity in 2022 results in a strong competition on the buy-side across all ticket sizes. To stay ahead of the competition, modern private equity funds had to adapt by creating new value propositions targeting the sellers.

The new generation of private equity emerges more and more as a sophisticated day-to-day business partner with industry know-how and dedicated portfolio management expertise. All of this creates an unprecedented value proposition for business owners.

Flexibility

One of the main benefits of selling to a private equity firm is the flexibility they can offer in deal structures and investment horizons. Unlike strategic buyers, who may have more specific strategic goals and integration plans, private equity firms are often more flexible in how they structure deals. For example, a private equity firm may be willing to offer more favorable terms for the seller, such as allowing them to retain some equity in the company.

Quick process execution

Private equity firms are able to execute deals quickly is that they have a more streamlined decision-making process. Because private equity firms are typically smaller and less bureaucratic than strategic buyers, decisions can be made more quickly and with less red tape. This allows private equity firms to move more quickly through the deal process, from initial due diligence to negotiating and closing the transaction.

Private equity firms also tend to be more focused on the deal itself than strategic buyers. Strategic buyers may have a number of competing priorities and may be less willing to move quickly on a deal if it doesn’t fit within their broader strategic plans. Private equity firms, on the other hand are more motivated to move quickly and efficiently on a deal.

Focus on Growth

Another benefit of selling to a private equity firm is their focus on driving growth and creating value in portfolio companies. Private equity firms typically have a lot of experience in identifying and executing on growth strategies, whether that be expanding into new markets, investing in new products or improving operational efficiency. Because their goal is to generate a strong ROI for their investors, private equity firms are incentivised to help the companies in their portfolio grow and improve. For business owners looking to expand and improve their operations, this can be a big advantage over selling to a strategic buyer, who may not prioritise the same level of growth and value creation.

Retaining Management and Employees

Private equity firms may be more inclined to retain existing management and employees, particularly if they believe that the existing team can help drive growth and create value. This can be a big advantage for business owners who want to ensure that their team is taken care of after the sale. In some cases, private equity firms may even incentivise management and employees with equity or other incentives to help drive growth and create value. Strategic buyers may be more focused on integrating the acquired company into their existing operations, which can lead to more changes in management and employee structures.

Return on Investment

While both strategic buyers and private equity firms aim to generate a return on their investment, private equity firms typically have a more focused approach to value creation and may be better positioned to execute on a specific growth strategy. This can result in a higher return on investment for business owners who sell their companies to private equity firms with a re-participation stake. Private equity firms are typically very focused on generating a strong ROI for their investors, which can lead them to be more proactive and aggressive in driving growth and creating value in portfolio companies.

Maintaining company’s legacy

When a company is acquired, the new owner often has the power to make significant changes to the business. This can include changes to the company’s operations, management and culture. In some cases, this can lead to the destruction of the company’s legacy and the erosion of the brand and reputation that the business has built over time. However, private equity firms have a reputation for being more focused on preserving a company’s legacy and maintaining its culture after a takeover, compared to strategic buyers.

Private equity firms may be more focused on the long-term success of the company than on short-term gains. This means that they are often more willing to invest in the company’s infrastructure and operations, rather than making significant changes to try and achieve quick wins. This can help to preserve the company’s legacy by ensuring that the business continues to operate in the same way it has in the past, while also investing in its future growth and success.

Another factor that may contribute to private equity firms being more inclined to preserve a company’s legacy is their focus on value creation. Private equity firms typically acquire companies with the goal of generating a strong return on investment for their investors. This means that they are more focused on driving growth and creating value in the business, rather than making significant changes that could erode the company’s legacy and reputation. In many cases, preserving the company’s legacy can be a key part of the strategy for creating value, as it can help to maintain customer loyalty and brand recognition.

Finally, private equity firms may be more likely to work collaboratively with the existing management team and employees of the company, rather than imposing their own management and culture on the business. This can help to preserve the existing culture and values of the company, while also ensuring that the management team and employees remain engaged and motivated after the takeover. By retaining the existing management team and employees, private equity firms can also benefit from their knowledge and experience, which can be essential in driving growth and creating value in the business.

“Overall, there are always pros and cons when choosing between a financial or strategic investor. However, we see that the private equity paradigm indeed shifts away from a pure valuation proposition for the sellers to a more flexible, growth-driven value proposition”, says Fabian Kröher, Executive Director at Winterberg Group.

Source: Preqin

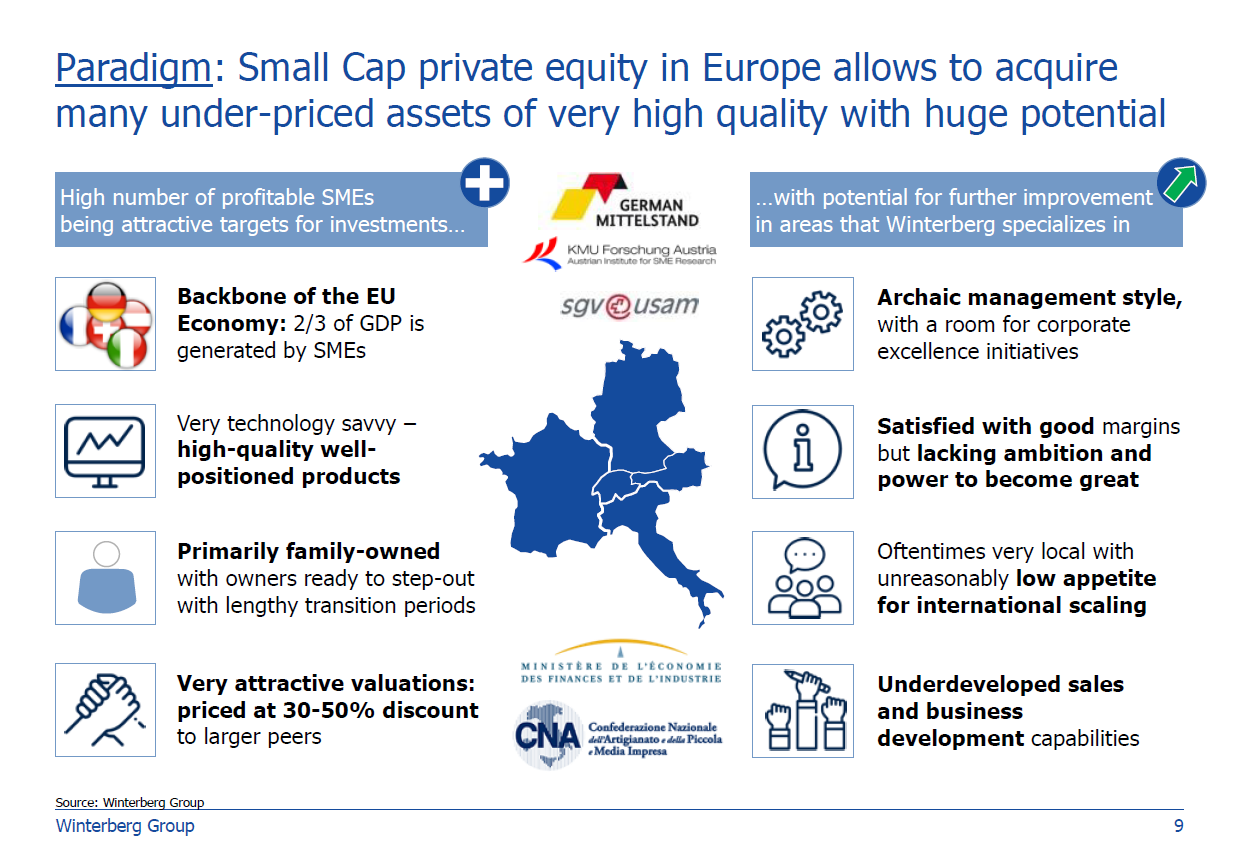

The DACH region (Germany, Austria, and Switzerland) is known for its robust economy and strong industries. One important feature of this region’s economy is the prevalence of small and medium-sized enterprises (SMEs), also known as Mittelstand. These companies are critical to the region’s economic growth, as they account for the majority of employment and GDP in the area. As a result, investing in these companies is of great importance, not only for the investors but for the region’s economy as a whole.

Mittelstand Landscape in the DACH Region

The term Mittelstand refers to small and medium-sized companies in the DACH region with revenues ranging from a few million euros to a few hundred million euros. These companies are often family-owned or managed with a long-term focus on growth and profitability. The Mittelstand landscape in the DACH region is vast, comprising over 3 million companies, and they employ around two-thirds of the workforce.

Mittelstand companies in the DACH region are known for their high-quality products, technological innovation and excellent customer service. These companies are also highly specialsed and dominate specific niche markets, which gives them a competitive advantage. For example, German Mittelstand companies are known for their engineering expertise, which allows them to provide high-tech products and services to various industries.

Challenges faced by Mittelstand companies

Despite Mittelstand’s strengths, these companies face several challenges that can hinder their growth and profitability. One significant challenge these days is access to capital, as many Mittelstand companies have limited financial resources. These companies often rely on bank loans or internal financing, which at current interest rates, can limit their ability to invest in research and development, expand operations or acquire new companies.

Another challenge is the lack of digitalisation, as many Mittelstand companies have not fully adopted digital technologies. This can limit their ability to compete with larger companies and reduce their efficiency and productivity. Additionally, many Mittelstand companies struggle with succession planning, as they are often family-owned or managed. Finding a suitable successor can be challenging, particularly if the family members are not interested in taking over the business.

Investing in Mittelstand

Investing in Mittelstand offers several benefits. Firstly, these companies are often stable and profitable and have a long-term focus, therefore resulting in high visibility on potential returns. Secondly, despite each individual company’s strength, there are usually many inefficiencies that can be solved by merging similarly-sized companies across the value chain. Thirdly, SMEs tend to be traded at a discount (so-called size discount to larger peers), therefore offering better returns with the same fundamentals.

However, investing in Mittelstand companies also comes with risks. These companies are usually highly specialised and have sophisticated products or service offerings, therefore requiring the owner’s presence and involvement in daily operations. Sometimes, when we at Winterberg look at Mittelstand targets, we can’t see the business post-acquisition without the selling shareholder. In combination with Seller’s age, this can be problematic, as it is sometimes impossible to motivate 70-year-old owners, who have been working for their family business for dozens of years, to perform at 150% of their capacity once they have cashed out. The majority of selling shareholders don’t want to be operationally involved after the sale, which raises the chicken and egg problem for us and usually results in a failed deal.

Valuation Multiples

When we talk about Mittelstand valuations, in Q1 2023, based on the processes we are involved in, we see the overall range of 4x – 8x EBIT as the basic case for Enterprise Value. With such a range, the sellers may have more than a 2x difference in the purchase price, so we thought that it would be insightful for sellers to learn which major factors influence the valuations.

Industry and Market Conditions

Specific industry and market conditions can have a significant impact on a company’s valuation multiple. Companies in high-growth industries such as technology or healthcare often have higher valuation multiples compared to companies in slow-growth industries like industrials. As with any other product, the market conditions, such as supply and demand, also affect the valuation multiples. If there are many buyers and few sellers in a specific industry, the valuation multiples may be higher.

Growth and Profitability

Small-sized companies with strong growth prospects and profitability often have higher valuation multiples. Investors are willing to pay a premium for companies with high growth potential, as they expect to earn higher returns in the future. Companies with a track record of generating strong profits and cash flows can also attract higher valuation multiples.

Size and Scale

The size and scale of a small-sized company can impact its valuation multiples. Smaller companies may have lower valuation multiples due to higher risks and uncertainty compared to larger companies. As companies grow and achieve scale, they may benefit from economies of scale, which can lead to higher profitability and cash flows, resulting in higher valuation multiples.

Business Model

A particular company’s business model also affects its valuation. Project-based revenue, high customer concentration, high supplier concentration, vulnerable value chain position, high working capital requirements and high capital intensity – these factors lower the valuation multiple as they are associated with higher risks.

Management and Leadership

The quality of management and leadership can also impact the valuation multiples of small-sized companies. We prefer to invest in companies with competent and experienced management teams, who have a track record of successfully growing and managing businesses. Companies with strong management and leadership teams that are not dependent on the selling shareholders may have higher valuation multiples due to the reduced risk of investment.

Deal Structure and Risk Sharing

Risk-sharing mechanisms in the forms of earn-outs, re-participation, vendor loans and the like, which drags the selling shareholders to participate in the company’s future usually increase the overall valuation of the company, as part of the purchase price is deferred in nature.

Country risk

While DACH is usually considered a homogenous region, it is not like this when it comes to valuations. Before Credit Suisse’s merger with UBS was announced, it was visible, that German SMEs had a discount compared to Swiss SMEs, while Austrian SMEs had a small discount on German SMEs. We are yet to see where the dynamics post-CS deal will lead the markets.

Winterberg Group investments in Mittelstand

At Winterberg, we focus on Mittelstand investments since 2017. Following successful deals in different sectors, we are on the watch for players with EBITDA in the range of 1-5 million EUR with a strong product and services portfolio, experienced management and robust market position.

“There are many specialised players within the DACH Mittelstand that contribute to addressing major problems of the future. Mittelstand’s unique features allow us not only to achieve attractive returns but also to make a positive impact on our society and environment.”

Fabian Kröher, Executive Director at Winterberg Group

Source: Winterberg Group

How increased interest rates impact the Private Equity industry?

After an unprecedentedly long period of close-to-zero interest rates, central banks have been aggressively hiking interest rates to control inflation. This has impacted the global markets, and the private equity industry is no exception.

In general, higher interest rates result in lower returns and lower competition, which leads to lower asset prices in Private Equity. In theory therefore, this should be a zero-sum game for the investors over a long period, as increasing interest rates should be balanced off by lower multiples and visa-versa. The market corrections may however take years. In the short run therefore, increasing interest rates may have the following impact on the private equity industry:

Lower returns: Private equity firms often rely on borrowing money to finance their investments, and higher interest rates can increase the cost of borrowing. This can result in lower returns on investment, as more money is required to service the debt.

Reduced deal activity: Higher interest rates can make it more difficult for private equity firms to finance acquisitions, leading to reduced deal activity. This can lead to fewer investment opportunities and slower growth for private equity firms.

Portfolio company performance: Higher interest rates can increase the cost of debt financing for portfolio companies, which can put pressure on cash flow and profitability. This can negatively impact the overall performance of the private equity firm’s portfolio.

Decreased competition: As borrowing becomes more expensive, private equity firms may have fewer competitors, which can lead to lower valuations for assets and decreased returns on investment.

Impact on exit strategies: Higher interest rates can impact exit strategies for private equity firms, as it can be more difficult to sell assets in a high-interest-rate environment. This can result in longer holding periods and reduced returns on investment.

Who is impacted?

Strategic PE players vs. leverage-driven

The devil is in the detail. Some of the traditional Private Equity competitors noticeably struggle in the current environment. “The key decisive factor is the source of the value-creation. We keep seeing our competitors entering deals with up to 80% leverage with adjustable rates and basically no growth plan. Obviously, they are in trouble now”, says Fabian Kröher, Executive Director at Winterberg Group.

Meanwhile, more hands-on PE players, implementing a wide range of organic and non-organic growth drivers, for instance via a buy-and-build strategy, are not expected to be negatively impacted in any significant way by the current turmoil. Key growth drivers for more hands-on Private Equity funds mostly include strong growth plans, extraction of synergies between multiple entities, access to new markets, value-add expertise in more efficient management, and others. As a result, the return rates are much less sensitive to any changes in interest rates.

Large-cap vs. Small-cap

We at Winterberg Group also see a big disparity in how the changes in interest rates differently impact larger-cap transactions vs. the smaller-sized environment.

Larger acquisition targets with an established track record have a much larger debt-carrying capacity. As a result, we saw ridiculously high multiples in the past, which were purely justified by vast debt amounts at low interest rates. Those funds also face minimum IRR thresholds, which are now becoming more and more difficult to achieve. As a result, we see funds being forced to hold onto assets much longer, due to min. return thresholds, which are not going to be realized in the event of an exit. Strong competition on the buy-side at the same time is not fully compensating for the valuation multiples correction, forcing the buy-side participants to overpay for the assets. As a result, we see less deals getting to the market at acceptable prices.

Smaller-cap Private Equity deals, in contrast, feature lower leverage in the capital stack, limiting the impact of the overall interest rate hikes on the returns. In combination with lower competition, the current market conditions create a much more buyer-friendly environment.

Shifting credit landscape (alternative credit providers vs traditional banks)

The combination of increasing regulatory standards (Basel I – IV) with very low-interest rates made the credit leverage finance business for traditional banks extremely unattractive. Especially in the lower-size segment, the transaction execution expenses on the bank’s side often exceeded the potential interest rates, they would get in return. In addition, increasing KYC requirements and strict risk policies made banks very slowly in their processes, becoming a potential bottleneck of a transaction from the Private Equity’s point of view.

All of the above created an unprecedented growth of private debt providers emerging. Indeed, the global Private Debt market has more than tripled in the last 7 years. The USPs of Private Debt providers are clear: quick execution, less strict credit policies, and high leverage amounts in exchange for a higher interest rates, compared to a traditional bank. Given the overall ultra-low interest rate environment, this seemed like an attractive trade-off for the Private Equity industry.

Source: Reuters

However, we believe that the competition between traditional banks and Private Debt providers is expected to intensify in the coming years, as Private Debt providers will have to adapt to growing delinquency rates and as a result, adapt their credit policies. At the same time, the spike in interest rates makes traditional credit leverage finance more attractive for the banks, who are expected to ramp up their deal-sourcing efforts soon. “We already see the competition between different lenders intensifying. We’ve never seen that many players proactively reaching out to us with very flexible financing solutions”, says Fabian Kröher, Executive Director at Winterberg Group.

Moreover, with the increasing difficulties to generate attractive returns in a high interest environment, Private Equity funds will need to put a larger emphasis on the overall cost of capital, which shall favour the traditional banks.

When we at Winterberg Group acquire Mittelstand companies in the DACH region, we encourage the selling shareholders to re-participate with a minority stake in the company. Why? The answer is simple – on the one hand, we want to share a portion of our risks. On the other hand, for owners, it’s usually a good way to invest part of the proceeds from a sale and continue to build up their wealth.

From our experience, ways of re-participation may vary on a case-by-case basis, but are generally one or another form of the following three mechanics:

Re-investment: The business owner can re-invest some or all of the proceeds from the sale of the company into the acquiring company (AcquiCo or the Fund). This can be done through investing cash proceeds from a sale in a new fund that will hold the acquiring company.

Equity rollover: In an equity rollover or in-kind contribution to the Fund, the business owner exchanges their ownership in the acquired company for ownership in the acquiring company. This allows the owner to maintain their stake in the business and benefit from future growth.

Earn-out: An earn-out is a contractual arrangement where a portion of the purchase price is contingent on the future performance of the acquired company. One way of looking at this, is that a part of a purchase price is simply deferred, while others may consider it as an investment mechanism. Ultimately, the seller receives less cash at closing with an opportunity to receive more if the business performs well. Technically it is equal to re-investing cash or company shares in the Fund.

In certain cases, we offer a combination of the above options which helps us and the selling shareholders to achieve a mutually beneficial result. Not all deals are created equal, so it’s important for us that the business owners carefully consider the re-participation mechanism that they’ve been offered.

Typical Seller’s perspective on re-participation and earn-outs

Typically, the seller will be open to a reasonable re-participation and/or an earn-out, provided that key aspects are well and transparently documented in the SPA. However, the most frequent questions are the following:

Q: Are the milestone targets reasonably achievable in a reasonable time period?

A: We usually base our KPIs based on the Seller’s business plan and/or historical performance of the business. Therefore, the Sellers are definitely capable of evaluating the possibility of a business plan achievement.

Q: How can the seller make sure the buyer doesn’t operate the business in a way that minimise or eliminates the earnout payments?

A: It has never been and never will be our intent to undermine business performance in any possible way. That’s not wise to shoot your own business in the leg, as the business needs to have a compelling story for the next buyer. If the concern is strong, we usually provide a performance metric range, so that the seller receives a portion of the deferred payment even in cases when the company performs worse than planned. In addition to that, re-participating sellers usually have customary board representation rights and are participating in the operations, so they have enough leverage to see the true performance.

Q: Is the amount of the potential deferred payments significant enough to delay the seller getting all cash up front?

A: All deals are different, and all sellers have different circumstances and plans. In deals we typically do, the earn-out and re-participation components are within a range of 10 to 30% of the purchase price.

Why is it important for us that the selling shareholders re-participate?

Overall, the re-participation of selling shareholders is usually beneficial to both us and the selling shareholders, as it helps to drive growth and profitability for the company.

First off, re-participation aligns interests: When selling shareholders re-participate in the company, they have a stake in the ongoing success of the business. This aligns their interests with those of the financial investor and management team.

Secondly, and this is critical for Mittelstand, expertise and experience: The selling shareholders, who are usually owning the business for generations, often have significant expertise and experience in the industry and with the company. This is valuable to the financial investor and management team as they work to grow the business.

Another reason is confidence in the business: If the selling shareholders are willing to re-participate in the company, it is a positive signal to us that they have confidence in the business and its future prospects.

How does the common market practice look in 2023?

In terms of the DACH market, some agencies regularly solicit feedback from a wide number of M&A advisory firms on their market outlook. One of the recent reports by Firmex, for example, suggests that M&A advisors reported that deal volume remains constant with half of the respondents forecasting deal volume in the coming three months to increase. At the same time, over half of the M&A firms questioned observed a growing gap between prices asked by sellers and prices buyers are willing to pay. The gap in value expectation is being increasingly filled by special mechanisms to narrow the gap in price expectations, like re-investment and earn-out mechanisms. Four out of ten M&A advisors said that earn-outs have become much more common. That certainly resonates with our own experience here and we see this as a necessary instrument in times of uncertainty which we definitely have today.

Source: Firmex

Water is essential for human survival, and ensuring a secure and reliable water supply is of paramount importance. In Germany, the Water Security Law (Wassersicherstellungsgesetz) aims to provide emergency water supply to cities in times of crisis, ensuring the population’s uninterrupted access to clean drinking water. The law has been designed to provide a framework for local authorities to ensure that water supply can be maintained even in the face of extreme weather events, natural disasters, or other crises.

The Water Security Law stipulates that the Federal Government is responsible for equipping cities with necessary machines, devices or pumps to ensure the uninterrupted supply of water to the population. The law emphasizes the need to provide one pump per approximately 1,500 inhabitants. This guideline is based on the assumption that a single pump can supply water to about 3,000-5,000 people, depending on the pump’s capacity and the distribution network’s design.

The law’s implementation is the responsibility of the local authorities, who must develop and maintain emergency water supply plans to ensure that the population’s water needs are met during a crisis.

The Water Security Law is just one part of the broader framework that ensures water supply security in Germany. The country has a robust water management system, which includes the Water Resources Act (Wasserhaushaltsgesetz), the Drinking Water Ordinance (Trinkwasserverordnung), and the Federal Water Act (Wasserhaushaltsgesetz). These laws regulate water use, protect water resources and ensure drinking water meets the highest standards of quality.

In addition to legal frameworks, Germany also has a well-established water infrastructure that provides reliable access to drinking water to its population. The country’s water supply system is decentralised, with more than 6,000 water supply companies managing the water distribution network. This decentralised system ensures that the water supply is less vulnerable to disruptions than centralised systems.

Despite the robust legal framework and well-established infrastructure, Germany is not immune to water crises. In recent years, the country has faced extreme weather events, such as droughts and floods.

Source: https://worldwarzero.com/

Recent droughts in Germany: when there’s not enough water, it does not necessarily mean there’s not enough drinking water.

The hot and dry years in the 1990s, and particularly the year 2003 have shown that Germany can be hit by low water and drought, despite being in the temperate climate zone. In Germany this exceptionally long dry and hot phase has led amongst other things to increased risk of forest fires, losses in the agricultural sector, restrictions on inland waterway traffic and on the operating times of thermal, hydroelectric and nuclear power plants. The reinsurance company Munich Re estimated the costs of the heat wave of 2003 in Germany at more than 1.2 billion EUR. Others report an agro-economic impact of this drought event for Germany of 1.5 billion EUR, and 15 billion EUR for all of Europe. However, the supply of drinking water was not threatened during 2003.

The period 2014-2018 was a dry period in large parts of Europe, the worst multi-year soil moisture drought during the last 253 years (1766-2018) in especially Central Europe. In Germany, an exceptionally hot summer happened in 2015, when almost 75% of the area of Germany was under at least moderate drought in July. During August 2015, the total area under drought decreased, but the areas of extreme and exceptional drought conditions increased to 22% and 5%, respectively.

The degree to which a region is hit by changes in runoff depends strongly on the size of the change and on the initial situation. Especially regions that presently have an unfavorable water balance and low runoff, such as e.g. the central regions of Eastern Germany, can be strongly impacted by climate change. In these regions, the shift of precipitation from summer to winter leads to further decreases in summer runoff, when the situation has already been difficult in arid years and causes further water shortages. Even if the results vary between climate models, there is considerable evidence that climate change will increase the risk of arid periods and droughts.

Flood and drought conditions in five large river basins in Germany (covering 90% of the German territory) were estimated from a large number of regional climate model projections. The results for 2061-2100 (compared with 1961-2000) show that many German rivers may experience more frequent occurrences of current 50-year droughts. During the summer there will be much less water available than at present. Between 1990 and 2080 the runoff in summer, depending on the climate model used and the emission scenario considered, will show a decrease of up to 43%. Rivers with a markedly Alpine runoff regime will also be affected by other components, such as accelerated melting of glaciers or permafrost soils and changes in the stability and thickness of snow cover.

However, since Germany’s drinking-water supplies are obtained largely from locally available groundwater resources and only partly via bank filtration or from surface waters (for example, reservoirs), no fundamental problems in drinking-water supplies are expected even under changed climatic conditions. On the other hand, regional scarcities might occur in areas that suffer extensive periods of drought.

Source: @Ralf Hirschberger/dpa/picture-alliance

Floods: when too much water puts availability of drinking water in danger.

On the night of July 14-15, 2021 the floods hit the Ahr Valley in southwestern Germany. Within a day, the floods turned many people’s lives upside down. Heavy rains transformed small rivulets and streams in the states of Rhineland-Palatinate and North Rhine-Westphalia into torrents. More than 180 people lost their lives and around 17,000 people lost all their possessions. At least 60,000 houses and 28,000 companies were destroyed altogether, causing damages of at least 33 billion EUR.

Last year, Germany marked 20 years since Elbe floods. In 2002, dozens were killed, hundreds injured and tens of thousands left homeless when torrential rains caused the Elbe and other rivers in eastern Germany to burst their banks in one of Europe’s worst natural disasters. In August 2002 a heavy rainfall in Central Europe caused record-breaking floods in the Czech Republic, Austria and Germany. One of the first cities affected was Passau, in Bavaria. The Danube reached 10.8 meters, its highest level since 1954. On August 17, the Elbe and Weisseritz rivers flooded parts of Dresden’s historic city center affecting the Zwinger Palace. In 2002, the floods caused major damage across Germany. It left behind destroyed roads, bridges and railroad tracks, as here near Riesa. Houses and dikes were damaged, and harvests were ruined. The Elbe flood of 2002 is still considered the most expensive natural disaster in German history. The total damage amounted to 11.6 billion EUR.

Flooding can lead to contamination of water sources, damage to water infrastructure and disruption of water supply networks. One of the primary ways that floods can impact drinking water availability is through the contamination of water sources. As rivers and lakes overflow, the pollutants and debris enter the water. This includes sewage, chemicals and other hazardous materials, which can contaminate the water and make it unsafe for drinking. Another way that floods can impact drinking water availability is through damage to water infrastructure. Floods can cause significant damage to water treatment plants, water supply networks and water storage facilities. This damage can result in disruptions to the water supply and can take time to repair, leaving people without access to clean drinking water.

The Water Security Law, along with other water management laws and regulations, aims to address these challenges and ensure that the population’s uninterrupted access to clean drinking water is ensured even in times of crisis.

Source: Helmholtz Centre for Environmental Research

Emergency water supply market: an interesting niche

The emergency water supply market can essentially be split into two large segments: (1) emergency water wells and (2) emergency water equipment.

The market for emergency water wells in Germany is a relatively small but important sector of the water supply industry. Emergency water wells are a critical source of water during times of crisis, when traditional water sources may be unavailable or contaminated. In Germany, emergency water wells are typically drilled into underground aquifers or other water-bearing rock formations. These wells can be equipped with pumps and filters to extract and treat water for drinking and other purposes. Emergency water wells can vary in size, depth and capacity, depending on the specific needs of the community or region they serve. Despite the relatively small size of the market, the demand for emergency water wells in Germany is expected to grow in the coming years. The Water Security Law as well as increasing frequency of extreme weather events and the need to ensure a reliable and safe water supply during emergencies drives the emergency water wells market. The market consists of a limited number of companies specializing in the design, drilling and maintenance of these wells.

As for the equipment part, there are various types of emergency water pumps and filters available, including portable pumps, submersible pumps and large-scale water pumps. These pumps are designed to be used in different situations and can range in capacity from small pumps that can deliver a few hundred liters per hour to large pumps that can deliver thousands of liters per minute. The pump and compressors sector belongs to the most important areas of mechanical engineering in Germany and is estimated at ca. 12 billion EUR in 2022. The market consists of a number of large players, as well as from the long tail of smaller producers of equipment, engineering and value-add distributor companies.

Winterberg Group in the context of emergency water supply market

Following successful execution of the Buy & Build strategy in water and wastewater treatment market in recent years, Winterberg Group aims to create a holding in the emergency water supply market by consolidating niche Mittelstand companies in this sector. We are on the watch for players with EBITDA in the range of 1-5 million EUR with strong product and services portfolio, experienced management and robust market position.

“The German Mittelstands boasts many highly specialised players which in some way contribute to battle the water crisis. We would like to invest into this macro trend to not only make attractive returns, but also to help countering the effects of this crisis on our country and our lives.”

Fabian Kröher, Executive Director at Winterberg Group

Winterberg Group, one of the leading Buy & Build specialists in small caps are launching a new platform in Switzerland with the acquisition of Senectovia Medizinaltechnik AG. The newly founded Healthcare Holding Schweiz AG aims to become a leading provider in the distribution and services of medical technology.

Baar, Switzerland – December 2021

Healthcare Holding Schweiz AG has successfully acquired Senectovia Medizinaltechnik AG, a leading rental (pay-per-use) provider of anti-decubitus medical mattresses and beds for hospitals across Switzerland.

This is the first step in the execution of the company’s buy-and-build strategy in the Swiss healthcare market. The strategy implies the acquisition of a core asset that will serve as a nucleus foundation for further acquisitions in the field of MedTech Distribution and Services. By adding similar but complementary assets to the core platform Healthcare Holding will achieve cost and revenue synergies while keeping it in the structure of a group of companies rather than a fully integrated corporate.

“We are immensely proud of this first step in our acquisition strategy. This milestone not only solidifies our presence in the Swiss MedTech market but also paves the way for a productive and successful future with Senectovia. We believe that our combined expertise and resources will lead to significant advancements in the quality and efficiency of medical services provided to hospitals, nursing homes and practices across Switzerland,” stated Fabian Kroeher, Executive Director of Winterberg.

“We are pleased that Senectovia is now in capable hands. This acquisition will undoubtedly support its ongoing development and ensure its prosperous future. We are confident that Healthcare Holding Schweiz AG will maintain the high standards of service and innovation that Senectovia is known for, and this partnership will help drive further growth and success,” noted Michael Lienhart, Member of the Executive Board, Chairman of the Board of Senectovia Medizinaltechnik AG.

Healthcare Holding Schweiz AG strives to focus on value-added services in order to be able to provide a sustainable value proposition for customers. The company’s strategy is to become the leading player in Swiss MedTech Distribution and Services, constantly promoting innovative solutions and expanding its portfolio.

About Senectovia Medizinaltechnik AG

Senectovia Medizinaltechnik AG specializes in the distribution and maintenance of products for decubitus prophylaxis and therapy, patient mobility and obesity therapy. The product range includes medical mattresses and aids for positioning and mobilizing patients.

About Healthcare Holding Schweiz AG

Healthcare Holding Schweiz AG is a prominent player in the Swiss Medtech services and distribution space, dedicated to expanding its portfolio through strategic acquisitions and collaborations. Committed to innovation and customer satisfaction, the company endeavors to set new benchmarks in the healthcare industry through cutting-edge solutions and unparalleled service.

About Winterberg Advisory GmbH

Winterberg Advisory GmbH based in Gruenwald, Germany, manages Private Equity investment funds which are primarily active in Small and Midcap Buy and Build platforms.

About Winterberg Group AG

Winterberg Group AG based in Zug, Switzerland is an independent family office investing in Small and Midcap Private Equity as well as selectively in Ventures, Real Estate and other asset classes.

For media inquiries, please contact galina.derkacheva@winterberg.group

Note to Editors: Please credit Winterberg Group for all references to provided quotes and information.

For further information about Senectovia Medizinaltechnik AG visit www.senectovia.ch

For further information about Winterberg Group AG and Healthcare Holding Schweiz AG, please visit www.winterberg.group

This press release is prepared and distributed by Winterberg Advisory GmbH on behalf of Healthcare Holding Schweiz AG.