Over the last years, the private equity landscape has witnessed a surge in increasingly aggressive capital structures for leveraged buyouts. Driven by the pursuit of higher returns, numerous private equity firms have sought to maximize their investments by employing excessive debt to finance acquisitions. However, this aggressive approach has come with significant risks, leading to concerns among banks and private debt providers. With strongly increasing interest rates, more and more aggressive leveraged buyouts begin to tumble. As a result, these financial institutions are now dedicating more efforts to portfolio management, emphasizing the importance of resilient business models and sustainable capital structures to secure successful transactions.

Aggressive Capital Stack

In recent years, the competitive nature of the private equity industry has prompted firms to take on higher levels of debt, hoping to magnify their returns. This practice, known as overleveraging, entails increasing the debt-to-equity ratio in an acquisition deal. Although overleveraged investments may deliver substantial returns in the short term, they expose companies to heightened financial risks and hamper their long-term growth prospects.

Consequently, a growing number of portfolio companies have faced difficulties servicing their mounting debts, leading to potential defaults and bankruptcies. As banks and private debt providers have been at the forefront of financing these deals, the increased risk exposure has made them more cautious in their approach to lending.

Increasing Portfolio Management efforts

To mitigate the risks associated with overleveraged investments, banks and private debt providers have increased their portfolio/debt management efforts. Rather than just focusing on originating new transactions, they are now heavily engaged in restructuring and turnaround activities. This heightened focus on portfolio management has been catalyzed by the lessons learned from the aftermath of the 2008 financial crisis. Many financial institutions faced severe losses due to the collapse of overleveraged investments during that period. As a result, there is now a greater emphasis on proactive monitoring, early identification of red flags and a hands-on approach to managing portfolio companies.

The Role of Resilient Business Models

One of the critical factors that banks and private debt providers now consider when evaluating potential investments is the resilience of the target company’s business model. A resilient business model demonstrates the ability to adapt to changing market conditions, economic downturns and disruptions in the industry.

A company with a resilient business model is better equipped to weather economic storms, maintain steady cash flows and service its debt even during challenging times. This resilience is derived from diversification of revenue streams, the scalability of operations, and a customer-centric approach. By investing in companies with robust business models, financial institutions aim to minimize the risk of default and increase the likelihood of a successful investment outcome.

„Resilient business models and sustainable capital structures are not merely buzzwords but prerequisites for long-term success in the private equity domain. Companies that prioritize adaptability and financial prudence are better equipped to thrive amid uncertainties”, says Fabian Kröher, Executive Director of Winterberg Group AG.

Sustainable Capital Structures: A Key to Long-term Success

Another crucial aspect that banks and private debt providers now emphasize in investment decisions is the establishment of sustainable capital structures. Sustainable capital structures strike the right balance between debt and equity financing, ensuring that the company can comfortably manage its debt obligations without being burdened by excessive interest payments.

A sustainable capital structure reduces the risk of financial distress and allows the company to invest in growth initiatives, research and development, and operational improvements. It also provides the flexibility to weather economic downturns, avoiding the need for distress sales of assets or shares to meet debt commitments.

Conclusion

The past years have seen a notable increase in overleveraged investments in the private equity sector. In response to this trend, banks and private debt providers are now dedicating more efforts to portfolio management, prioritizing resilient business models and sustainable capital structures in their investment decisions. By emphasizing these factors, financial institutions seek to minimize risks, enhance the probability of successful investments, and support the growth and stability of their portfolio companies. As the private equity landscape continues to evolve, the lessons learned from the consequences of overleveraging are steering the industry towards a more cautious and sustainable approach to investment management.

„With increasing interest rates and increasing complexity of obtaining debt finance, we expect Private Equity players with a sustainable leverage structures and resilient investment strategy to prevail in the coming years„, says Fabian Kröher, Executive Director of Winterberg Group AG.

Introduction

Securing debt financing is a critical aspect of business growth and expansion. However, obtaining financing in the 5-20 million EUR range has become increasingly complex. This is primarily due to the structure of financial institutions, where finance tickets below 5 million EUR are handled by local branches, while deals above 5 million EUR typically require the involvement of leverage finance teams. Given the expensive cost structure of these teams, they tend to focus on deals above 20 million EUR, leaving a significant financing gap for mid-sized transactions. As a result, businesses are turning to private debt as a viable alternative, leading to its growing importance in the financing landscape.

The Implications for the Economy

The complexities surrounding debt financing in the 5-20 million EUR space have macro-level implications for the business landscape. Fabian Kröher, Executive Director of Winterberg Group, highlights these implications, stating, „The limited access to bank debt financing for mid-sized transactions has created a bottleneck in the market. This has hindered the growth and expansion of many businesses, leading to missed opportunities for job creation, innovation, and overall economic development.“

Inadequate financing options: The focus of leverage finance teams on larger deals leaves avoid in the availability of tailored financing solutions for mid-sized transactions. As a result, businesses in the 5-20 million EUR range struggle to find suitable funding options that align with their specific needs.

Hindered business growth: Without sufficient financing options, businesses face challenges in executing their growth strategies. The inability to access debt financing can limit their ability to pursue mergers, acquisitions and organic expansion opportunities, hindering overall business growth.

Reduced competition and market dynamics: The lack of accessible debt financing for mid-sized transactions can stifle competition within industries. This, in turn, may lead to market consolidation, limiting consumer choice and potentially impeding innovation and competitive dynamics.

The Growing Importance of Private Debt

In light of the limitations in traditional bank debt financing, private debt has emerged as a crucial alternative for businesses in the 5-20 million EUR range. Private debt providers offer specialised financing solutions, addressing the unique needs of mid-sized transactions. This alternative source of funding has gained prominence due to its flexibility, speed and ability to bridge the financing gap left by traditional banks.

Fabian Kröher explains, „Private debt has become increasingly important as a financing option for mid-sized transactions. Its tailored solutions and expertise in this specific market segment enable businesses to access the capital necessary for their growth plans.“

Tailored financing solutions: Private debt providers are equipped to structure financing solutions that align with the specific requirements of mid-sized transactions. This flexibility allows businesses to secure funding while maintaining operational control and minimizing equity dilution.

Specialised expertise: Private debt providers focus on understanding the nuances and challenges of mid-sized transactions. Their industry knowledge enables them to assess risk effectively and provide customised solutions that traditional banks may not offer.

Speed and efficiency: Private debt providers often have streamlined decision-making processes, enabling faster access to capital. This agility is particularly advantageous in competitive acquisition scenarios where timing is crucial.

Expansion of the capital market: The rise of private debt has expanded the overall capital market, providing businesses with additional options beyond traditional bank financing. This diversification of funding sources enhances market stability and resilience.

Conclusion

The complexities of obtaining debt financing in the 5-20 million EUR range present challenges for businesses seeking capital to fuel their growth. Traditional banks, with their expensive cost structures, often focus on larger deals, leaving mid-sized transactions underserved. However, the growing importance of private debt has filled this financing gap, offering businesses specialised solutions and expertise tailored to their needs.

Fabian Kröher emphasizes, „Private debt plays a vital role in addressing the financing challenges faced by mid-sized businesses. Its ability to bridge the gap left by traditional banks and provide tailored financing solutions positions it as a crucial alternative in the market.“

As businesses continue to seek debt financing in the 5-20 million EUR range, the private debt industry is poised to play an increasingly prominent role. Its flexibility, specialised expertise, and ability to fill the financing gap contribute to the overall growth and stability of businesses, fostering innovation, job creation, and economic development.

The DACH region, comprising Germany, Austria and Switzerland, has long been recognised as a hub for innovation and economic growth. With a stable political climate and a strong focus on research and development, the region has attracted significant private equity (PE) investments in recent years. This article will explore the top 10 critical trends shaping the DACH private equity landscape, from industry preferences to macro trends.

As a leading player in the DACH region, the Winterberg Group, co-founded by Fabian Kroeher, has been at the forefront of these investment trends. By understanding and adapting to the evolving dynamics of the market, Winterberg has successfully navigated the challenges and capitalized on the opportunities presented by these trends.

The Rise of Technology & Digitalization Investments

The DACH private equity landscape is witnessing a significant focus on technology and innovation. Start-ups and growth-stage companies in sectors such as fintech, artificial intelligence, health tech and e-commerce are attracting substantial investments. The Winterberg Group, led by industry expert Fabian Kroeher, has been actively funding innovative ventures in these sectors, positioning the company as a leader in DACH private equity.

The Shift Towards Sustainable and Impact Investing

Sustainability and environmental, social and governance (ESG) have become increasingly crucial in investment decision-making. Fabian Kroeher, Co-Founder and Executive Director of Winterberg Group, and his team have recognised the potential of incorporating ESG criteria into their investment strategy. As a result, more PE firms are looking for opportunities in sectors such as renewable energy, electric mobility and circular economy.

The Growing Popularity of Buy-and-Build Strategies

In recent years, there has been a growing trend toward buy-and-build strategies in the DACH private equity market. This approach involves acquiring a platform company and then adding on complementary businesses through subsequent acquisitions. Winterberg Group has successfully executed several such transactions, creating value by enhancing their portfolio companies‘ operational efficiency and market presence.

The Emergence of Industry 4.0 & Advanced Manufacturing

The fourth industrial revolution, or Industry 4.0, has led to a surge in investments in advanced manufacturing technologies in the DACH region. Private equity firms, including Winterberg, are targeting companies involved in advanced robotics, additive manufacturing and industrial IoT, as these technologies can potentially disrupt traditional manufacturing processes and create significant value for investors.

The Focus on Healthcare & Life Sciences

The DACH region is home to numerous world-class healthcare and life sciences companies. With an aging population and increasing demand for innovative healthcare solutions, private equity firms are keenly interested in this sector. Winterberg Group and Fabian Kroeher have identified opportunities in biotechnology, medical devices and digital health, which are expected to drive growth in the coming years.

The Expansion of Infrastructure & Real Asset Investments

As governments in the DACH region continue to emphasize infrastructure development, private equity firms are witnessing a growing trend of investing in infrastructure and real asset projects. These investments are particularly appealing due to their inherent characteristics of providing stable and long-term cash flows, making them a valuable addition to private equity portfolios. One notable participant in this burgeoning trend is Winterberg Group, which has actively engaged in various sectors such as transportation, energy and telecommunications infrastructure. By strategically allocating capital and expertise, Winterberg Group has seized opportunities in these areas to contribute to the region’s infrastructural growth and development.

The Preference for Small & Mid-sized Companies

Private equity firms in the DACH region increasingly gravitate towards small and mid-sized companies (SMEs) as their preferred investment targets. Winterberg Group and other prominent players seek out these enterprises due to their enticing growth prospects. These firms recognise that SMEs possess the potential for remarkable expansion and the possibility of making operational enhancements and facilitating market consolidation. Private equity investors can generate substantial value and propel sustainable long-term growth by establishing partnerships with such companies. Collaborating with SMEs enables these firms to leverage their expertise, capital and network to optimize the company’s operations, streamline processes and identify growth opportunities.

The Increasing Importance of Operational Expertise

As the private equity market becomes more competitive, firms emphasize operational expertise more to generate value within their portfolio companies. Winterberg Group, led by the visionary Fabian Kroeher, has emerged as a prominent player in this growing trend by adopting a hands-on approach. Their strategic approach drives operational enhancements and fosters synergies across their diverse investments. Winterberg Group recognises that more than providing financial backing is needed to stay ahead in the private equity landscape.

The Growing Role of Co-Investments & Club Deals

Co-investments and club deals, where multiple private equity firms collaborate on a single investment, are becoming more prevalent in the DACH region. This approach allows firms to pool their resources and expertise while mitigating risk and increasing the potential for higher returns. Winterberg Group has actively participated in such deals, reflecting its commitment to collaboration and innovation in private equity.

The Impact of Macro Trends on Investment Strategies

Environmental, Social and Governance (ESG) factors are increasingly critical in DACH private equity investments. Investors seek companies committed to sustainable practices, social responsibility and good corporate governance. Under the guidance of Fabian Kroeher, Winterberg Group emphasizes ESG integration throughout its investment portfolio, aligning financial returns with positive societal impact.

Final Words

The DACH private equity landscape is experiencing a range of noteworthy trends shaping the investment strategies of firms like Winterberg Group. By understanding and adapting to these trends, firms can capitalize on the opportunities they present and successfully navigate the dynamic market environment. As the DACH region continues to evolve, it is crucial for investors and industry players such as Fabian Kroeher, Co-Founder and Executive Director of Winterberg Group, to stay informed and agile to thrive in this competitive landscape.

“As demonstrated in this article, the DACH private equity market is experiencing a variety of investment trends, ranging from industry preferences to macro trends. By staying up-to-date on these developments and incorporating them into their strategies, private equity firms like Winterberg Group can continue to create value for their investors and portfolio companies.”, says Fabian Kroeher.

As climate change’s adverse effects continue to manifest globally, there has been a marked increase in Atlantic Ocean temperatures, currently three degrees hotter than historical averages. For private equity (PE) investors, the ramifications of such climatic changes are far-reaching and necessitate a rethinking of investment strategies. Climate adaptation – the process of adjusting to the current and expected future climate – is now an essential component of sustainable investing.

The Imperative of Climate Adaptation

Extreme climate change, typified by the warming Atlantic Ocean, is reshaping the global business landscape. Increased ocean temperatures impact global weather patterns, disrupt agricultural practices and increase the likelihood of catastrophic events such as hurricanes and flooding. These climatic shifts directly impact the assets held by PE firms, posing significant operational and financial risks.

At the same time, climate change also presents novel investment opportunities. As businesses and societies grapple with the challenge of adapting to our changing climate, new markets and industries are emerging. Companies developing innovative solutions for climate adaptation, such as renewable energy technologies, water management systems and sustainable agriculture, are increasingly attractive investment prospects.

Winterberg’s Take

Fabian Kroeher lends a compelling perspective on the subject of climate adaptation.

Kroeher stated, „At Winterberg, we recognise climate change as a reality, much like the stages in the grieving process. We experience shock, denial, anger, bargaining, depression, testing and finally acceptance. The last stage – acceptance – is where we currently stand in the face of climate change. Acceptance isn’t synonymous with resignation. It’s about acknowledging the reality and preparing ourselves to adapt accordingly. We, at Winterberg, are wise enough not to battle with the changes in climate. Instead, we align our investment strategy to support industries that are leading the charge towards climate adaptation. We do not swim against the tide, but with it. That’s our strategic pivot, our key to ensuring that our investments remain resilient and sustainable in the face of this inevitable change.“

We witness the urgency with which private equity investors must treat climate adaptation. Accepting the inevitability of climate change is not a sign of defeat; rather, it is the first step in strategising for a future that acknowledges this reality. By focusing on industries that foster climate adaptation, Winterberg and investors who follow their lead are paving the way towards a resilient and sustainable future.

The Risk and Opportunity Duality

For PE investors, the duality of risk and opportunity underlines the importance of climate adaptation. On the risk side, failing to consider climate impacts could lead to significant financial loss. Businesses may face operational disruptions due to extreme weather events, regulatory pressures as governments implement stricter environmental standards and reputational damage if they are seen as contributing to climate change.

Conversely, on the opportunity side, companies that successfully adapt to climate change can offer attractive investment opportunities. Those at the forefront of developing sustainable technologies, creating resilient supply chains or transitioning to low-carbon operations stand to benefit from the growing consumer and regulatory demand for environmentally friendly practices.

Navigating the Climate Adaptation Landscape

To navigate this challenging landscape, PE investors should incorporate climate adaptation strategies into their investment process. Here are a few critical steps to consider:

Climate Risk Assessment: PE investors need to assess the climate risks of potential investments comprehensively. This assessment should include understanding a company’s exposure to physical risks, such as extreme weather events, as well as transitional risks associated with moving to a low-carbon economy.

Integration of ESG Factors: Environmental, Social and Governance (ESG) criteria offer a robust framework for assessing a company’s sustainability performance. PE investors can use ESG metrics to identify companies that are proactively addressing climate adaptation and those lagging behind.

Active Engagement: PE investors can play a significant role in promoting climate adaptation by actively engaging with portfolio companies. This engagement could involve advocating for the implementation of climate resilience measures, supporting the development of sustainable products and services, and promoting transparency in climate-related disclosures.

Collaboration and Partnership: Climate change is a global problem that requires collective action. PE investors can collaborate with other stakeholders, including governments, non-governmental organizations and other institutional investors to support broader climate adaptation efforts.

The rising Atlantic Ocean temperature is a stark reminder of the reality of climate change. For PE investors, this environmental change necessitates a shift in focus towards climate adaptation. By considering climate risks and opportunities, integrating ESG factors, actively engaging with portfolio companies and promoting collaboration, PE investors can contribute to climate adaptation efforts and ensure the long-term sustainability of their investments.

Importance of Getting the Normalizations Right

The EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) holds a significant position as a key performance parameter. It serves as a metric to evaluate a company’s operational efficiency and profitability. However, there is probably only a few companies out there, where the reported accounting EBITDA shows the full picture of businesses operating result. In order to arrive at a meaningful EBITDA number (adjusted EBITDA), EBITDA is normalized for any aperiodic, non-recurring items. If normalized correctly, analysts can eliminate distortions caused by non-recurring or non-operational items, providing a clear picture of a company’s sustainable performance. However, if done incorrectly, the adjusted EBITDA can even disrupt the picture even further and lead to misleading conclusions about the performance of a company.

Common Acceptable Normalizations

When it comes to EBITDA normalisations, the focus is on identifying and adjusting for items that are non-recurring, non-operational, or non-market standard. These normalizations aim to present a more accurate representation of the company’s core business operations. Let’s delve into some common acceptable normalizations:

Non-market standard owner’s compensation: especially in the smaller cap segment, where ownership and management is not separated, owners tend to compensate themselves either strongly above market-related rate, or below. In order to account for this item accurately, total owner’s compensation should be added back to the EBITDA and average market-rates should be deducted.

Personal & non-market costs: it is common practice, especially in smaller cap high margin businesses to account in the P&L for personal costs of senior management and owners via company accounts. The idea behind this logic, is to minimize the tax exposure by reducing taxable income on the P&L.

The correct way to account for this is to fundamentally understand:

if such costs are market-standard

if such costs would continue to exist in case of a takeover / merger.

If both of the cases are not true, one should specifically adjust for such items. In the contrary case not.

“This, together with non-market owner compensation is by far the most common adjustment to EBITDA we see. It is crucial to use common business sense to understand, if such costs are indeed non-market standard and if the new buyer will have to carry them to the same degree. Otherwise it can get pretty creative”, says Fabian Kröher, Executive Director at Winterberg Group.

Non-Operating Income and Expenses: EBITDA focuses on operational performance, so non-operating items, not relating to the business activity of the company, including any foreign exchange impact, dividend income from investment activities, income/losses from any activities, which are not going to be part of the business in case of a potential merger/takeover should be adjusted.

Non-arms-Length Revenues and Expenses: when evaluating the core value of the business, it is important to evaluate, which part of revenues and EBITDA are related with associated entities. In certain cases, the company may book non-market-related services and revenues, which may have an impact on the EBITDA. Such items, should be adjusted accordingly, if all contracts would have not been there, in case of a different ownership/management.

Real estate item: in case where the entity is the owner of real estate facilities, the target company may not display any rent expenses in the P&L, or display non-market related costs. Real estate and companies however are valued at different quasi multiples. Therefore, in order to accurately account for the real-estate, for the Company: one should add back, if any, existing rent payments in favor of the company and deduct a market-standard rent, which would have been paid, in case of a different ownership. For the real estate: one needs to divide the resulting market-standard net operating income (NOI) by a market-standard capitalization rate.

Restructuring Costs: Expenses incurred during major restructuring efforts, such as severance payments, facility closures, or reorganization charges, are typically considered non-recurring. These costs should be normalized to provide a clear picture of ongoing operations.

Mergers and Acquisitions: Transaction-related costs, including legal fees, due diligence expenses, and integration costs, are often excluded from EBITDA. Such expenses are specific to the merger or acquisition and are not reflective of the company’s day-to-day operations.

Other One-Time Events: Certain extraordinary events, such as natural disasters, litigation settlements, or regulatory fines, have a significant impact on a company’s financials but are not indicative of its ongoing operations. Normalizing for these events helps present a more accurate financial picture.

It’s important to note that these normalizations should be verifiable. They must be supported by appropriate documentation, such as financial statements, disclosures, or management explanations, to ensure transparency and credibility.

Non-Common Normalizations

While some normalizations are widely accepted, caution must be exercised when dealing with non-common normalizations. These are items that may be used to manipulate EBITDA artificially or obscure the true financial health of a company.

Let’s explore a few examples:

Operating Lease Adjustments: Some companies try to book operating leases below the EBITDA line to artificially boost their EBITDA. By doing so, they understate their lease expenses, resulting in an inflated EBITDA figure. Proper normalization requires adjusting these lease expenses to reflect their true impact on the business.

Release of Reserves: Companies occasionally release reserves, which are funds set aside to cover future contingencies, to artificially increase EBITDA. These reserves are meant to address potential losses or expenses and do not represent real value created by the company. Adjusting for such releases is crucial to obtain an accurate EBITDA figure.

Questionable Revenue Recognition: Some entities may engage in aggressive revenue recognition practices, recognizing revenue prematurely or inflating sales figures to enhance EBITDA. Identifying and normalizing these practices ensures a more reliable assessment of a company’s performance.

Bad Business Performance: although claimed to be a one-off, the company may face difficulties with the overall industry trend, internal personnel problems etc. Such items indeed should not be normalized for, as the potential new owner may indeed face similar risks after a takeover.

Non-Standard Accounting Practices: Companies may employ accounting tricks, such as capitalizing expenses that should be treated as operational costs, to manipulate EBITDA. Normalizing for such practices involves adjusting the financials to align with industry standards and common business sense.

Conclusion

“EBITDA is a valuable metric for assessing a company’s operational performance. However, to make informed decisions, it is crucial to normalize EBITDA by eliminating distortions caused by non-recurring, non-operational, or non-market standard items”, says Fabian Kroeher, Executive Director at Winterberg Group.

By following the do’s and don’ts of EBITDA normalizations, analysts can ensure a more accurate representation of a company’s sustainable performance. Transparency, verifiability, and adherence to accounting standards play vital roles in achieving reliable EBITDA figures, empowering investors and stakeholders with the insights needed for informed decision-making.

As the global community continues to face the challenge of climate change, the transition from fossil fuels to renewable energy sources has become a top priority. In Germany, the energy transition, or „Energiewende,“ is well underway, aiming to achieve a sustainable, low-carbon energy system by 2050. Key drivers of this transition include the expansion of renewable energy, increased energy efficiency, and the gradual reduction of greenhouse gas emissions. Small and medium-sized enterprises (SMEs) have a crucial role in this energy shift, and private equity firms, such as the Winterberg Group, are stepping in to provide the necessary financial and strategic support.

This article will explore how private equity impacts and supports SMEs in Germany’s energy transition, focusing on the Winterberg Group and its Co-Founder and Executive Director, Fabian Kroeher.

The Growing Importance of SMEs in Germany’s Energy Transition

As Germany works towards meeting its ambitious climate goals, SMEs have become increasingly important in driving progress. These smaller, agile companies are at the forefront of developing innovative technologies and services contributing to a more sustainable energy system. SMEs account for over 99% of all businesses in Germany, employ over 50% of the workforce and account for more than 55% of the country’s GDP.

The energy transition presents significant opportunities for SMEs, such as:

Developing renewable energy technologies, including solar, wind and biomass.

Creating energy-efficient buildings and infrastructure.

Offering smart grid solutions and energy storage systems.

Providing clean transportation options, like electric vehicles and public transport.

By seizing these opportunities, SMEs can create new jobs, foster economic growth and contribute to a more sustainable future for Germany.

The Role of Private Equity in Supporting SMEs

Given the importance of SMEs in Germany’s energy transition, they must have access to the necessary resources and support. This is where private equity firms like the Winterberg Group come in. These firms provide much-needed capital to SMEs, allowing them to scale their operations, invest in research and development and bring innovative solutions to the market.

In addition to financial support, private equity firms often provide strategic guidance, helping SMEs to navigate the complex and rapidly evolving energy landscape. They bring their extensive industry knowledge and networks to bear, connecting SMEs with potential partners, customers, and suppliers and assisting with regulatory and market challenges.

Furthermore, private equity firms are increasingly focused on sustainability and environmental, social and governance (ESG) criteria. This means that, by partnering with private equity, SMEs can further align their business models with the energy transition goals and build long-term value for their stakeholders.

The Importance of SME Support

SMEs are a vital part of the German economy. They account for over 99% of all businesses in Germany, employ over 50% of the workforce and account for more than 55% of the country’s GDP. SMEs are also responsible for a significant share of innovation in Germany.

The energy transition is creating several challenges for SMEs. Renewable energy costs are still relatively high, and the regulatory environment is complex. SMEs may also need more expertise and resources to transition to a new energy market. PE firms can help SMEs overcome these challenges and succeed in the new energy market. PE firms can help SMEs grow and create jobs by providing capital, expertise, and networks.

Winterberg Group: A Leading Private Equity Firm in Germany’s Energy Transition

The Winterberg Group, co-founded by Fabian Kroeher, is a prime example of a private equity firm making a tangible impact on Germany’s energy transition. With a strong focus on sustainability and innovation, the Winterberg Group invests in SMEs driving positive change in the energy sector.

Fabian Kroeher – Co-Founder and Executive Director of Winterberg Group – brings a wealth of experience in the finance and energy sectors. His background and deep understanding of the challenges and opportunities presented by the energy transition make him a valuable partner for SMEs seeking to scale their operations and make a positive impact.

Under Fabian Kroeher’s leadership, the Winterberg Group has developed a reputation for identifying and nurturing promising SMEs in the energy sector. The firm’s portfolio includes companies operating in renewable energy generation, energy efficiency and clean transportation among other areas.

By providing financial backing, strategic guidance, and access to a broad network of industry experts, the Winterberg Group is helping SMEs to overcome barriers to growth and accelerate their contribution to Germany’s energy transition.

The Winterberg Group’s investment approach is characterised by its focus on innovation, sustainability, and value creation. The firm is committed to investing in businesses driving the energy transition by developing new technologies, products, and services. In addition, the Winterberg Group strongly emphasises environmental, social, and governance (ESG) factors, ensuring that its investments contribute to the broader goals of the Energiewende and a sustainable future.

Fabian Kroeher, Co-Founder and Executive Director of Winterberg Group has been a driving force behind the company’s success in supporting SMEs in the renewable energy sector as well as in other ESG sectors. His background in finance, coupled with his passion for sustainability and renewable energy, has enabled him to steer Winterberg toward strategic investments that positively impact the environment and the economy.

Final Words

Germany’s energy transition is a monumental task that requires the collaboration of all stakeholders, including the government, large corporations and SMEs. In this context, private equity firms like the Winterberg Group, play a crucial role in providing the necessary resources, expertise and support for SMEs to thrive.

By investing in and nurturing SMEs that drive innovation and sustainability in the energy sector, private equity firms are helping accelerate Germany’s transition to a cleaner, greener future. The Winterberg Group’s success stories demonstrate the transformative impact of private equity on SMEs and their contributions to the energy transition.

“As Germany continues on its journey towards a more sustainable energy system, private equity firms like the Winterberg Group, will remain essential partners for SMEs. Together, they will continue to push the boundaries of innovation, create new jobs and foster economic growth while contributing to a more sustainable future for Germany and the world.”, says Fabian Kroeher.

The Mittelstand companies in the DACH region (Germany, Austria, and Switzerland), characterised by their small to medium size and often family-owned operations, are essential to the economic stability of their respective countries. However, these firms frequently fly under the radar of many larger institutional investors. Yet, for those with strategic foresight, these very enterprises offer a wealth of opportunity. A notable exponent of this perspective is Winterberg Group which is laser-focused on Buy & Build investment strategy.

The backbone of the DACH region’s economy, Mittelstand companies blend stability, resilience and niche market domination, often powered by an unrivalled degree of specialised knowledge. These attributes, along with their substantial employment creation and export potential, make them significant contributors to the regional GDP and societal stability. The Buy & Build investment strategy, focusing on the acquisition of a company that subsequently serves as a platform for further acquisitions, has proven to be incredibly potent within the Mittelstand universe. The DACH region, teeming with highly specialised, often complementary companies, is ripe for this approach.

Our Managing Partner, Fabian Kröher, shed some light on why this strategy has been so successful:

„The Buy & Build strategy aligns perfectly with the Mittelstand culture. These enterprises are often at the forefront of innovation, demonstrating extraordinary resilience in niche markets. With each strategic acquisition, we can integrate new product lines, broaden market reach or bolster existing capabilities, resulting in a stronger, more versatile entity. Essentially, we’re capitalising on the inherent strengths of these Mittelstand companies – their stability, innovative potential and profound market knowledge serve as the ideal foundation for growth.“

The returns stemming from this approach in the DACH region have been nothing short of remarkable. A well-executed Buy & Build strategy can spur significant revenue and EBITDA growth, create meaningful economies of scale and strengthen market positioning, ultimately enhancing the appeal of the combined entity for future exit opportunities, be it via a sale to financial investor or a strategic player.

Buy & Build strategy is inherently capable of mitigating the risks that are typical for Mittelstand

Succession Planning: Many Mittelstand companies are family-owned, often managed by founders or their descendants. The problem arises when the current management grows old or wants to retire. It’s not always guaranteed that the next generation will be willing or capable to take over. There may also be disputes among family members over leadership. Inadequate succession planning can lead to leadership gaps, business disruption, or even the sale or closure of the company. If there’s a lack of suitable successors in the family, a Buy & Build strategy could help. When we buy the company, if the need exists, we bring in professional management. This helps ensure a smooth transition and continued growth, without the need for family succession. The ongoing succession challenges faced by many Mittelstand owners, with impending retirement and no obvious successors. This dynamic offers an added opportunity for investors, like Winterberg Group, implementing a Buy & Build strategy, as these owners may be more inclined to sell to an investor who guarantees their legacy’s ongoing success.

Digital Transformation: Digital transformation involves using digital technologies to create or modify existing business processes and customer experiences to meet changing business and market requirements. While it provides opportunities to innovate and improve efficiency, it also poses challenges. Many Mittelstand companies may lack the necessary technical skills or financial resources. Failure to successfully transform can lead to lost competitive advantage, inefficiencies and lower profitability. We provide both financial resource and technical expertise to drive the company’s digital transformation. This would help the company stay competitive and increase efficiency without needing to develop these capabilities in-house.

International Competition: Globalisation has expanded markets, but it has also increased competition. Companies worldwide can offer similar products or services, sometimes at lower costs due to factors like cheaper labor or raw materials. This can put significant pressure on Mittelstand companies‘ revenues and profitability, especially those that are highly specialised in a particular niche. A Buy & Build strategy could help companies scale and expand their operations more rapidly, helping them compete more effectively on the global stage. With more resources and a broader reach, they can better face off against international competitors.

Supply Chain Risks: Global supply chains can be disrupted by various events such as political instabilities, trade disputes, natural disasters or pandemics. Such disruptions can lead to increased costs, delays, or inability to deliver products or services. Mittelstand companies may lack the resources or expertise to manage these risks effectively compared to larger, multinational firms. Winterberg brings expertise in supply chain management and risk mitigation strategies gathered during our Managing Directors’ prior expertise in top Strategy Consulting firms. Moreover, a larger, more diversified company may have a more resilient supply chain, with more options for sourcing materials and distributing products.

Economic Conditions: A company that’s part of a Buy & Build strategy can better weather economic downturns due to its greater size and diversification. It may also have more resources to hedge against economic risks, such as fluctuations in interest and exchange rates.

The potential of Mittelstand companies in the DACH region is immense. For investors like Winterberg Group, that recognise the inherent value in these enterprises and have mastered the Buy & Build strategy, the opportunity for exceptional returns is not only possible but likely. Winterberg Group’s success underscores the effectiveness of this approach in the vibrant and promising segment of the DACH market.

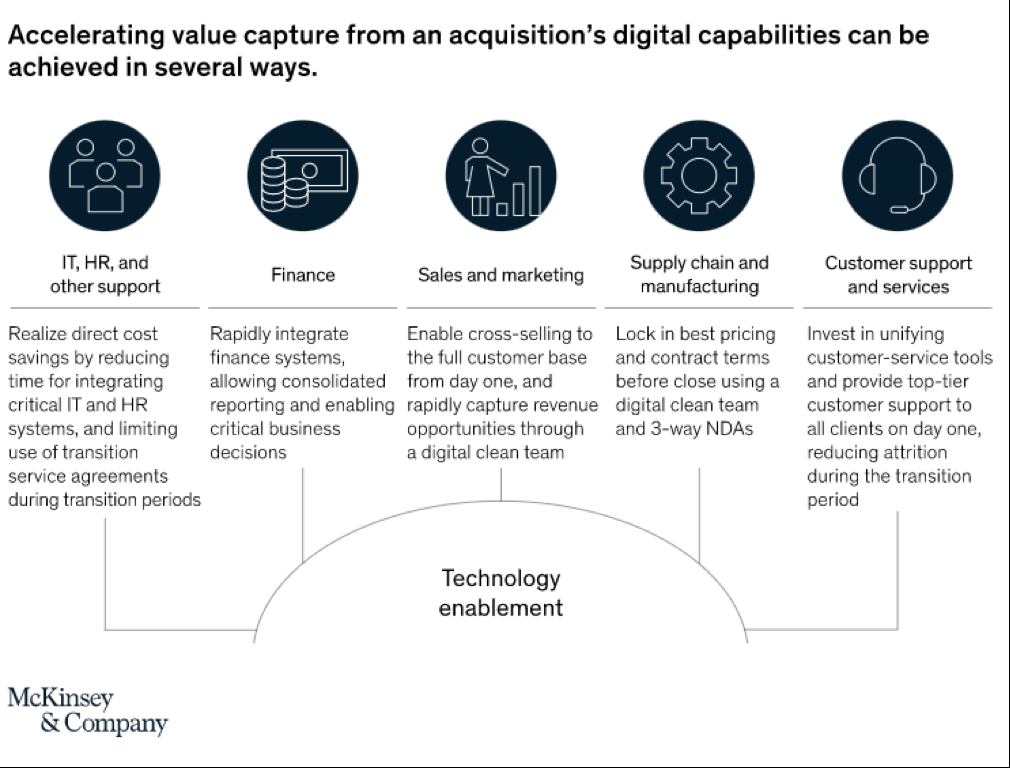

The world of mergers and acquisitions (M&A) and private equity (PE) has undergone a significant transformation in recent years, driven by the rapid advancement of digitalisation. Digital technologies have improved various aspects of these industries, including deal sourcing, matchmaking, due diligence, valuation, and parts of the post-merger integration.

Streamlining sourcing and matching

Digitalisation enables the collection and analysis of vast amounts of data, providing valuable insights that aid in the matchmaking process. Through data analytics, dealmakers can identify patterns, similarities, and potential synergies between companies. By leveraging data-driven intelligence, M&A and PE professionals can identify the most suitable counter-parties based on factors such as market positioning, customer profiles, financial performance, and growth potential. Moreover, digital tools offer sophisticated search and filtering capabilities that enable professionals to narrow down potential counter-parties based on specific criteria. This enables advisors to identify perfectly-matched companies based on industry, geographic location, financial metrics, growth rates, and other relevant factors. This targeted approach helps match buyers with sellers that align with their strategic objectives and investment criteria, saving time and effort in the process and enabling foremost advisors to address the best possible buyers significantly outside their usual network. As a result, digital channels, foremost online deal platforms, accounted for more than 20% of the deal-sourcing activities in 2022, up from 5% in 2016.

Automation of Due Diligence

Data analytics plays a vital role in the due diligence process by enabling companies to extract meaningful insights from large volumes of data. Traditionally, due diligence involved a manual review of documents and financial statements, which was time-consuming and prone to human error. With data analytics, companies can now automate the analysis of financial data and other relevant information. Such automated data analytics systems employ advanced algorithms to analyse various data sources for inconsistencies. By scanning through these data sets, these systems can quickly identify potential red flags that warrant closer scrutiny. Red flags can encompass financial irregularities, legal or regulatory non-compliance, operational inefficiencies, or other indicators of risk. These automated systems are designed to flag inconsistencies, outliers, and patterns that may raise concerns during the due diligence process. Automated data analytics systems can also assess compliance with regulatory requirements. By cross-referencing the target company’s activities against relevant laws and regulations, these systems can identify potential violations or gaps in compliance. As a result, foremost larger M&A transactions can be completed more cost-effectively.

Improving post-acquisition integration

Digitalisation plays a crucial role in post-merger integration and value creation. Advanced project management tools, collaboration platforms, and automation technologies enable smoother integration of systems, processes, and cultures. Especially if the acquisition needs to fit into a larger operating group, digital data solutions significantly simplify portfolio management efforts. By consolidating and aligning data, organisations gain a holistic view of their operations, financials, and customer information, facilitating better decision-making and the identification of synergies.

Furthermore, digital tools enable efficient collaboration and communication among teams involved in the integration process. Cloud-based project management software and virtual meeting platforms foster real-time collaboration, regardless of geographical location. This transparency and cross-functional teamwork accelerate the integration process. Digitalisation also allows for process automation, reducing manual effort and increasing efficiency. Organisations can utilise robotic process automation and workflow automation tools to streamline repetitive tasks, freeing up resources to focus on strategic integration initiatives.

“We see the importance of digitalisation efforts, when it comes to creating additional value for our portfolio companies, especially when it comes to identifying cross-synergies between different companies. Without sophisticated data tools, we’d probably miss out on quite a few synergies”, says Fabian Kroeher, Executive Director at Winterberg Group.

Source: McKinsey&Company

Improving deal quality

Digitalisation can significantly improve deal quality in M&A transactions by increasing transparency on both the buyer and seller sides. Transparency plays a crucial role in reducing the number of buyers who lack the financial capability to fund the deal and sellers who are reluctant to sell. On the buy-side, digitalisation allows potential acquirers to showcase their financial strength and credibility. Online platforms and databases provide access to information about a buyer’s financial history, track record, and available funds. This transparency helps filter out buyers who may not have the necessary financial resources to complete the transaction, ensuring that serious and capable buyers are involved in the deal process.

Similarly, on the sell-side, digital platforms could enable sellers to convey their intent to sell and provide relevant information about their company’s financials, operations, and growth prospects. This transparency can ensure that only sellers who are genuinely interested in selling their business participate in the M&A process, reducing time wasted on negotiations with sellers who are not committed to a deal. By leveraging digitalisation, M&A professionals can conduct thorough background checks, verify financial capabilities, and assess the seriousness of both buyers and sellers. This leads to improved deal quality as it minimises the likelihood of wasted efforts, failed negotiations, and disappointing outcomes.

“Overall we still see quite a few processes, where sellers don’t really intend to sell or buyers, who enter processes with no funds. We really hope that the overall deal quality can further improve through implementing digital processes – otherwise, it gets pretty frustrating from time to time”, says Fabian Kröher, Executive Director at Winterberg Group.

Conclusion

The digitalisation of the M&A and PE field has unleashed a wave of innovation, transforming traditional processes and unlocking new opportunities. The current level of implementation helps buyers and sellers to find each other easier, have more efficient due diligence, as well as improve portfolio management efforts for private equity players. However, there are little to no solutions in the market to help improve the deal quality. Nonetheless, the future of M&A and PE lies in further digitalisation and further process streamlining.

The world of alternative investments is vast and encompasses many asset classes. Two of this space’s most prominent investment strategies are Private Equity and Venture Capital. These asset classes have unique characteristics, risks and potential rewards for limited partners (LPs), i.e. investors in Private Equity and Venture Capital funds. In this article we will explore the performance of Private Equity versus Venture Capital for LPs.

Understanding Private Equity and Venture Capital

Before diving into the performance comparison, it’s essential to understand the fundamental differences between Private Equity and Venture Capital.

Private Equity

Private equity refers to investments in non-publicly traded private companies. These investments often involve significant capital infusions to help companies grow, restructure or improve their operations. Private equity firms typically acquire controlling stakes in these companies and work closely with management to create value for all stakeholders.

Venture Capital

Venture Capital is a type of Private Equity focused on investing in early-stage, high-growth potential startups. Venture capitalists provide financing, strategic guidance and networking opportunities to help these startups scale and achieve success. The investments in Venture Capital are often smaller and more speculative than those in Private Equity, as the companies receiving funding are typically at an earlier stage in their development.

Performance Comparison: Private Equity vs. Venture Capital

Several factors come into play when comparing the performance of Private Equity and Venture Capital for LPs.

1. Returns

Historically, Private Equity has consistently generated higher returns than Venture Capital. According to the Cambridge Associates US Private Equity Index, the 10-year annualised return for Private Equity was 13.7% as of Q2 2021, while the 10-year annualised return for Venture Capital was 11.9%. Other sources see an even wider spread between the different types of Private Equity (Fund-of-funds, Growth, Buyout and other) and Venture Capital, such as the analysis depicted below.

However, this does not mean that Venture Capital investments are inherently less attractive – the risk-return profile is different, with Venture Capital investments carrying higher upside potential and risks.

2. Risk

Venture capital investments are inherently riskier than Private Equity investments. Early-stage companies face numerous challenges, such as product-market fit, market adoption and competition. As a result, many startups fail, and Venture Capital investors must rely on a few successful investments to generate most of their returns.

By contrast, Private Equity investments typically involve more established companies with proven business models and cash flows. While risk is still involved, Private Equity investors can often mitigate these risks through active management and operational improvements.

3. Diversification

Both Private Equity and Venture Capital investments can provide valuable diversification benefits for LPs. These asset classes have historically exhibited low correlations to traditional asset classes, such as stocks and bonds, which can help reduce overall portfolio risk.

However, the level of diversification within each asset class can vary. Venture capital investments are often more concentrated in specific sectors, such as technology or healthcare, while Private Equity investments can be more broadly diversified across industries.

4. Liquidity

Private equity and Venture Capital investments are illiquid, meaning they cannot be easily bought or sold like publicly traded stocks. Investment horizons for both asset classes typically range from five to ten years, which can pose challenges for LPs who require liquidity.

Winterberg Group’s Approach: A Balanced Strategy

At Winterberg Group, we recognises the distinct characteristics of Private Equity and Venture Capital investments. While we are focusing on Private Equity, we have developed a balanced approach to maximize returns while mitigating risks for our LPs.

1. Sector Focus

Winterberg Group strategically invests in high-growth sectors to capitalise on market trends and opportunities. By focusing on industries such as technology, healthcare, water, certification and sustainability, Winterberg Group is well-positioned to benefit from the growth potential of these industries.

2. Active Management

Winterberg Group takes an active approach to managing its investments. By working closely with portfolio companies, we can help drive operational improvements, enhance efficiencies and unlock value. This hands-on approach is a crucial differentiator for the Winterberg Group, as it allows them to generate value from their investments beyond mere capital infusions.

Fabian Kroeher, Co-Founder and Executive Director of Winterberg Group, brings a wealth of knowledge and experience to the table. With a deep understanding of the investment landscape, Fabian Kröher and his team have demonstrated a consistent ability to identify attractive investment opportunities, conduct thorough due diligence and execute value-enhancing strategies.

3. Diversification

Winterberg Group understands the importance of diversification for their LPs and seeks to provide a balanced mix of Private Equity and Venture Capital investments in their portfolio. This approach allows us to benefit from the high return potential of Venture Capital investments while also enjoying the relative stability of Private Equity investments.

4. Selectivity

The Winterberg Group is highly selective in choosing its investments. We conduct thorough due diligence on potential investment opportunities to ensure we align with the firm’s strategic objectives and growth potential. This disciplined approach helps Winterberg Group mitigate risks and maximize returns.

Final Words

In conclusion, Private Equity and Venture Capital offer unique benefits and risks for limited partners. While Private Equity investments tend to provide more stable returns and involve less risk, Venture Capital investments offer higher growth potential but with increased risk. The proper allocation between these asset classes depends on an LP’s specific investment objectives, risk tolerance and diversification needs.

“The Winterberg Group has developed a balanced approach to investing in Private Equity and Venture Capital. By focusing on high-growth sectors, active management, diversification and selectivity, we seeks to achieve an attractive risk-return profile”, says Fabian Kröher, Executive Director at Winterberg Group.

GDP: Recession is not happening

With the release of robust data for Q1 2023, there is growing optimism that Germany’s GDP may avoid a decline in 2023, thus averting a recession.

The global economic landscape, including issues with global supply chains, has improved significantly. However, despite this improvement, there remains a heightened level of uncertainty. Real income losses due to high inflation are expected to continue, which is likely to dampen investment spending and private consumption in the first half of the year.

As tighter monetary policies begin to take effect and a potential recession looms in the United States, anticipated to begin in the fourth quarter, any economic recovery later in the year is expected to be modest. Therefore, we tend to agree with forecasts for German GDP growth in 2023 to remain at 0%, although there have been increased upside risks since the beginning of the year.

In Chancellor Scholz’s government declaration on 27.02.2022, he argued that the shock caused by the Russian invasion of Ukraine marked a historic turning point, referred to as a „Zeitenwende“ in German. This term holds strong positive connotations in Germany, as it is reminiscent of the reversal associated with German reunification in 1989/90. However, the current „Zeitenwende“ is brought about by the actions of the country that had facilitated German reunification, and it signifies a significant shift. Russia’s attack has underscored that the socio-economic development with the prevalence of Western, liberal democracies has not reached a happy ending.

The implications of this historic turning point will play a crucial role in shaping social and economic developments particularly in the medium and long term. However, these implications are currently difficult to identify and understand, which may explain the cautious adjustments to policies and corporate strategies. These adjustments seem inconsistent with the intentions expressed in speeches and surveys, and this discrepancy has caught the attention of many observers.

Even for the more cyclical developments expected in the next 12 to 24 months, uncertainty looms large. Typically, during stable periods, cyclical fluctuations occur around a consistent trend, with uncertainty limited to minor variations in estimated trend growth. However, concerns now exist that the incline of the trend might become much shallower.

These uncertainties are impacting the behavior of market players, evident in more prudent spending and investment decisions, as well as the emergence of new priorities. Yet, these new priorities have not yet led to a pronounced reassessment of existing ones. The current „Zeitenwende“ coincides with a series of other reversals in areas such as monetary policy, climate policy, transport policy, and gradually deteriorating demographic trends. Consequently, budgetary constraints are likely to become more pressing, as already indicated by the ongoing budgetary debates among various ministries in preparation for next year’s federal budget.

CPI Revisions: Lower Inflation Level Fails to Alleviate Concerns

The comprehensive overhaul of Germany’s Consumer Price Index (CPI) for 2023 resulted in a notable decrease in the inflation level. For 2023, we now anticipate an annual average of around 6%, while for 2024, our forecast stands at 2-2.5%. These adjustments primarily reflect technical factors rather than a shift in our overall perspective on inflation dynamics.

We still expect a substantial decline in the headline inflation rate throughout 2023, thanks to significant energy price base effects. However, despite the „disinflationary“ influence stemming from energy, core inflation could remain persistently high during the first half of 2023 before gradually easing in the second half. We acknowledge the risk that robust wage outcomes and potential second-round effects may keep core inflation in the range of 5% or higher for an extended period.

Although the revised CPI indicates a lower inflation level, concerns persist regarding core inflation and its potential impact.

Source: Deutsche Bank “The German economy – one year after”

German Industry: Anticipating a Minor Setback in 2023, Automotive Sector Shows Signs of Recovery

It is expected that domestic production in Germany’s manufacturing industry will experience a slight decline of -0.5% in 2023 (compared to -0.4% in 2022). Considering the assumption of a moderate economic recovery in the Eurozone throughout 2023 and 2024, with the United States potentially facing a recession in the first half of 2024, domestic production in the German manufacturing sector could see a modest growth of 1% next year. However, this estimate would still place the output level 7% below the historical peak reached in 2018.

Once again, there is an expectation of a notable decrease in production within energy-intensive industries in 2023. The chemical industry might experience another double-digit decline (following a -11.6% decrease in 2022).

On a positive note, with the easing of supply problems for semiconductors and high demand backlog, the automotive industry could see a substantial 10% increase in domestic production. However, for other capital goods producers, we exercise caution. The mechanical industry’s production is projected to rise by 1% in 2023, while electrical engineering may experience a 3% increase due to a high order backlog.

In 2022, German producer prices for industrial products saw a significant average increase of over one-third. This marked the highest increase since the inception of the time series in 1949. However, starting in October 2022, producer prices began to decline on a monthly basis. With lower energy prices and a weaker order intake, this downward trend could persist for several more months. On average, producer prices may experience a slight decrease compared to the levels observed in 2022.

In contrast to energy-intensive industries, capital goods producers demonstrated stronger performance in 2022, despite facing supply shortages for intermediate goods. Electrical engineering witnessed a notable increase in domestic production, reaching 4.3%. This sector continues to benefit from heightened demand driven by structural trends like digitisation and investments in green technologies. Additionally, the accumulation of a high order backlog over the past years, resulting from ongoing disruptions in the supply chain, provided support. Mechanical engineering in Germany experienced a modest 0.6% rise in production in 2022. While the sector still maintains a substantial order backlog, new orders declined by 6% due to increased interest rates and economic uncertainty linked to the conflict in Ukraine.

The automotive industry in Germany reported its first output increase since 2017, with a growth of 3.1% in 2022. However, the production index remained 24% below the previous peak in 2017. Among all industrial sectors, the automotive industry faced significant challenges with supply shortages, particularly in semiconductors. Orders were canceled at the onset of the COVID-19 pandemic, and subsequent supply retrieval proved insufficient due to full capacity utilization in the semiconductor industry driven by higher demand from other sectors. These shortages, coupled with disruptions related to the conflict in Ukraine, weighed on German production in recent years. Although demand for new vehicles gradually recovered, the automotive industry continued to face supply chain issues. As of February 2023, the latest IFO survey revealed that 74% of automotive companies still reported shortages in intermediate goods, though this number has decreased from previous peaks.

Structurally, the shift towards electric mobility triggered reorganisation measures at various production sites in Germany, including suppliers, resulting in reduced available capacities. Furthermore, German automotive factories in the volume car segment encountered difficulties competing successfully with intragroup sites located in other countries. The 3.1% increase in domestic output in 2022 halted the previous downward trend, and a further recovery is expected in 2023 due to anticipated easing of supply chain disturbances.

The pharmaceutical industry witnessed the highest increase in production in Germany during 2022, with a growth rate of 5.1%. It has been the most dynamic industrial sector in terms of domestic output, with the production index surpassing 2015 levels by 23% (while total manufacturing experienced a decline of 3.3%). The increased prevalence of respiratory illnesses, including COVID-19, in Germany contributed to high demand for medications, leading to temporary shortages. Additionally, the pharmaceutical sector benefits from structural trends such as an aging society.

Swiss Perspective

“For us at Winterberg, despite recent bank runs, Switzerland remains to be a smaller yet more stable and resilient market. That is also reflected in macro forecasts by the leading research institutions.” – Fabian Kröher commented on a topic.

The macroeconomic outlook for Germany and Switzerland presents notable differences in terms of real GDP growth and inflation projections. Switzerland is expected to outperform Germany in terms of economic growth, with forecasted real GDP growth of 0.6% in 2023 and 1.4% in 2024. In comparison, Germany’s real GDP growth is forecasted to remain stagnant at 0% in 2023 and show a modest increase of 1% in 2024. This suggests a more favorable growth trajectory for Switzerland, indicating a stronger economic performance in the coming years.

Regarding inflation, Switzerland is projected to experience lower inflation rates compared to Germany. In 2023, Switzerland’s inflation is forecasted at 2.4%, while Germany is expected to face higher inflation at 6.1%. Looking ahead to 2024, Switzerland’s inflation is expected to decrease to 1.5%, whereas Germany’s inflation is projected to decline to 2.3%. These figures indicate that Switzerland is expected to maintain a relatively stable and lower inflation environment compared to Germany, suggesting potentially better price stability and cost management in the Swiss economy.

Overall, based on these projections, Switzerland appears to have a more favorable macroeconomic outlook in terms of real GDP growth and inflation compared to Germany. Switzerland is expected to achieve positive economic growth, albeit modest, and maintain lower inflation rates. In contrast, Germany is facing the challenge of minimal economic growth in the near term and higher inflationary pressures. These contrasting outlooks highlight the differences in the economic dynamics and policy environments of the two countries.